This Statement of Fair Tax Mark compliance was compiled in partnership with the Fair Tax Foundation.

This Fair Tax Mark Statement certifies that Atlas Translations Limited meets the requirements of the Fair Tax Mark’s – Solely UK-based Business Standard.

The Fair Tax Mark label is the gold standard of responsible tax conduct and certifies that a business:

- Seeks to follow the spirit, as well as the letter of the law;

- Shuns artificial or aggressive corporate tax avoidance; and

- Is transparent about profits made and taxes paid.

Tax contributions are the lifeblood of a flourishing society – funding essential services such as healthcare, education, policing and transport. Corporate tax avoidance doesn’t just rob public services of vital revenue, it also undermines the ability of businesses to compete fairly and reduces national productivity. Across the world, there is a growing community of Fair Tax Mark certified businesses who believe in responsible tax conduct, spanning small businesses, listed companies, co-operatives and social enterprises.

Tax Policy

Atlas Translations Limited (“we” / “the Company”) is committed to paying all the taxes it owes in accordance with the spirit of all tax laws that apply to its operations. We believe paying our taxes in this way is the clearest indication we can give of being responsible participants in society. We will fulfil our commitment to paying the appropriate taxes that we owe by seeking to pay the right amount of tax, in the right place, and at the right time. We aim to do this by ensuring we report our tax affairs in ways that reflect the economic reality of the transactions that we undertake during the course of our trade.

We will not seek to use those options made available in tax law, or the allowances and reliefs that it provides, in ways that are contrary to the spirit of the law. Nor will we undertake specific transactions with the sole or main aim of securing tax advantages that would otherwise not be available to us based on the reality of the trade that we undertake. The Company will never undertake transactions that would require notification to HM Revenue & Customs under the Disclosure of Tax Avoidance Schemes Regulations or participate in any arrangement to which it might be reasonably anticipated that the UK’s General Anti-Abuse Rule might apply.

We believe tax havens undermine the UK’s tax system. As a result, while we may trade with customers and suppliers genuinely located in places considered to be tax havens, we will not make use of those places to secure a tax advantage, nor will we take advantage of the secrecy that many such jurisdictions provide for transactions recorded within them.

Our accounts and tax filings will be prepared in compliance with this policy, and we will seek to provide all the information that users, including HM Revenue & Customs, might need to properly appraise our tax position.

Company Information

Atlas Translations Limited is a private company, limited by shares, and was originally established in 2002. We are an award-winning UK translation agency, providing professional and certified language services to businesses and individuals across more than 300 languages, including a full mix of language, translation, localisation, and transcreation services.

The Company is wholly owned and controlled by Clare Suttie.

Our registered office and head office address is: Censeo House, 6 St. Peters Street,

St. Albans, Hertfordshire, England, AL1 3LF.

Tax Information

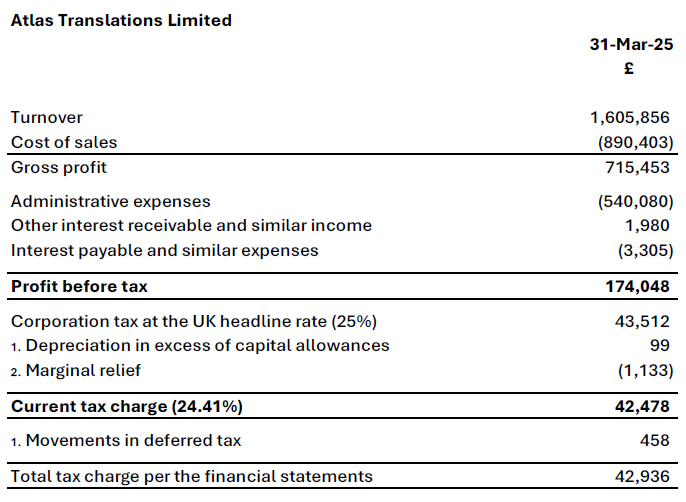

The Company’s profit before tax for the year ended 31 March 2025 was £174,048. The tax charge on this profit at the UK headline rate of 25% would be £43,512. Our actual current tax charge for the year was £42,478 at a rate of 24.41%; and the reasons for this being slightly lower than expected are explained below in the following tax reconciliation and accompanying footnotes:

- The accounting treatment of fixed assets differs from the tax treatment. For accounting purposes, fixed assets are depreciated over their useful economic lives. For tax purposes, there are specific rules to what can be claimed and when, depending on the type of asset (capital allowances). The differences between these treatments can often create a tax adjustment, which is only a timing difference, as eventually, the total capital allowances claimed on our tax returns will equal the total corresponding depreciation charged in our accounts on eligible assets.

We have made a provision for these temporary timing differences in our accounts (deferred tax). As at 31 March 2025, the Company had a deferred tax liability of £1,613 on its Balance Sheet. This liability will unwind in annual instalments over the economic lives of the assets that it relates to. During the current period, a charge of £458 was released to our Profit and Loss Account – creating a total tax charge of £42,936 (£42,478 current tax, plus £458 deferred tax charge) in our accounts. - From 1 April 2023, the main tax rate for companies with taxable profits over £250,000 increased from 19% to 25%. The small profits tax rate for companies with taxable profits below £50,000 stayed at 19%. For companies with taxable profits between these limits, the main tax rate is applied, but marginal relief is provided to gradually increase the Corporation Tax rate between the small profits rate and the main rate.

You can view and download our Fair Tax Mark (2025-2026) statement here.

You can view and download our Fair Tax Mark (2024-2025) statement here.

You can view and download our Fair Tax Mark (2023-2024) statement here.